Airbnb, Inc. (ABNB): Growth under elevated investment intensity

Airbnb, Inc. (ABNB): FY2025 FY analysis of earnings as of 2025-12-31

Source: company filings.

Access the complete report in PDF presentation format, with detailed charts and long-term value investing insights:

Download the full PDF presentation

Headline figures 2025, $ in bn

Business description

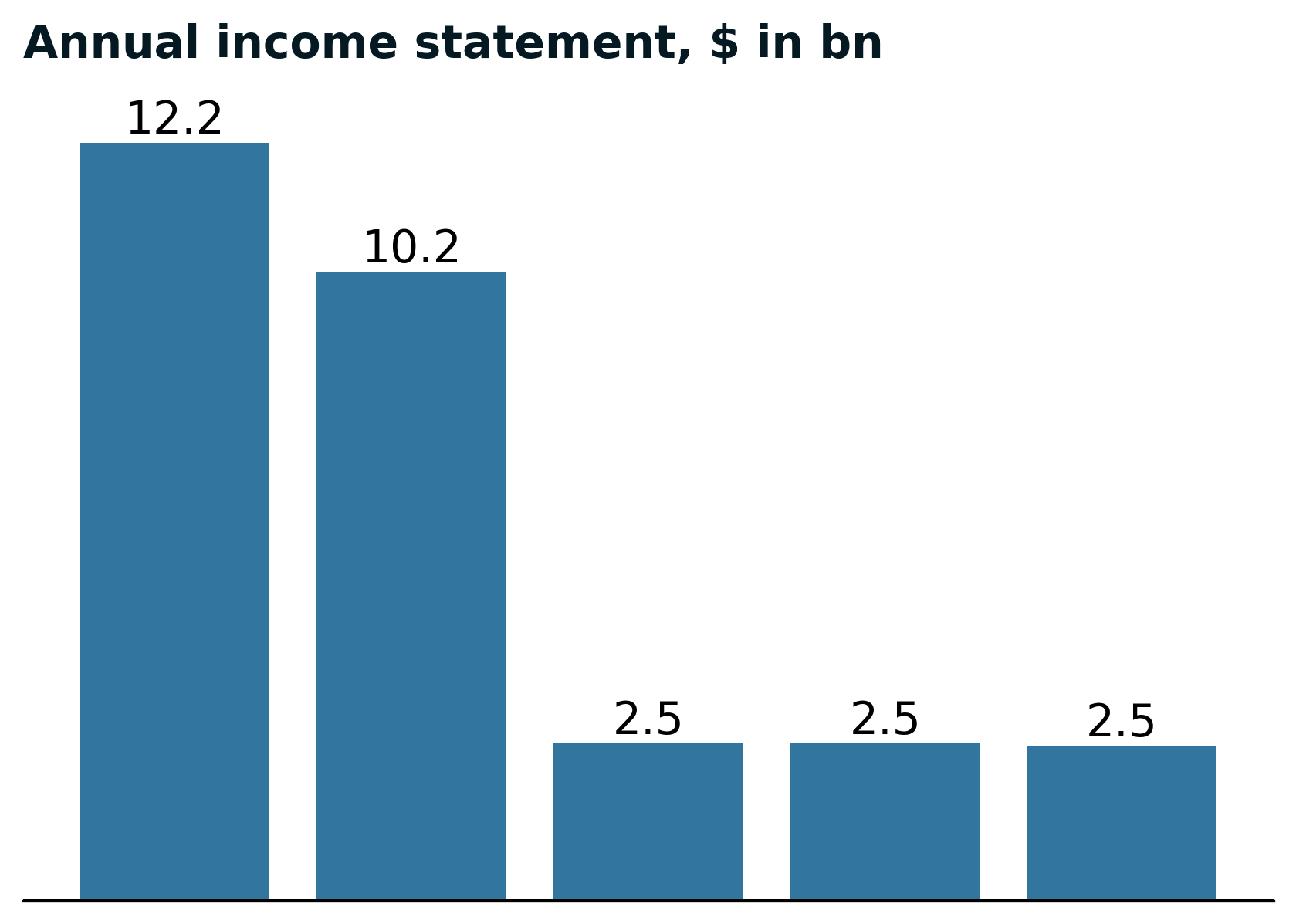

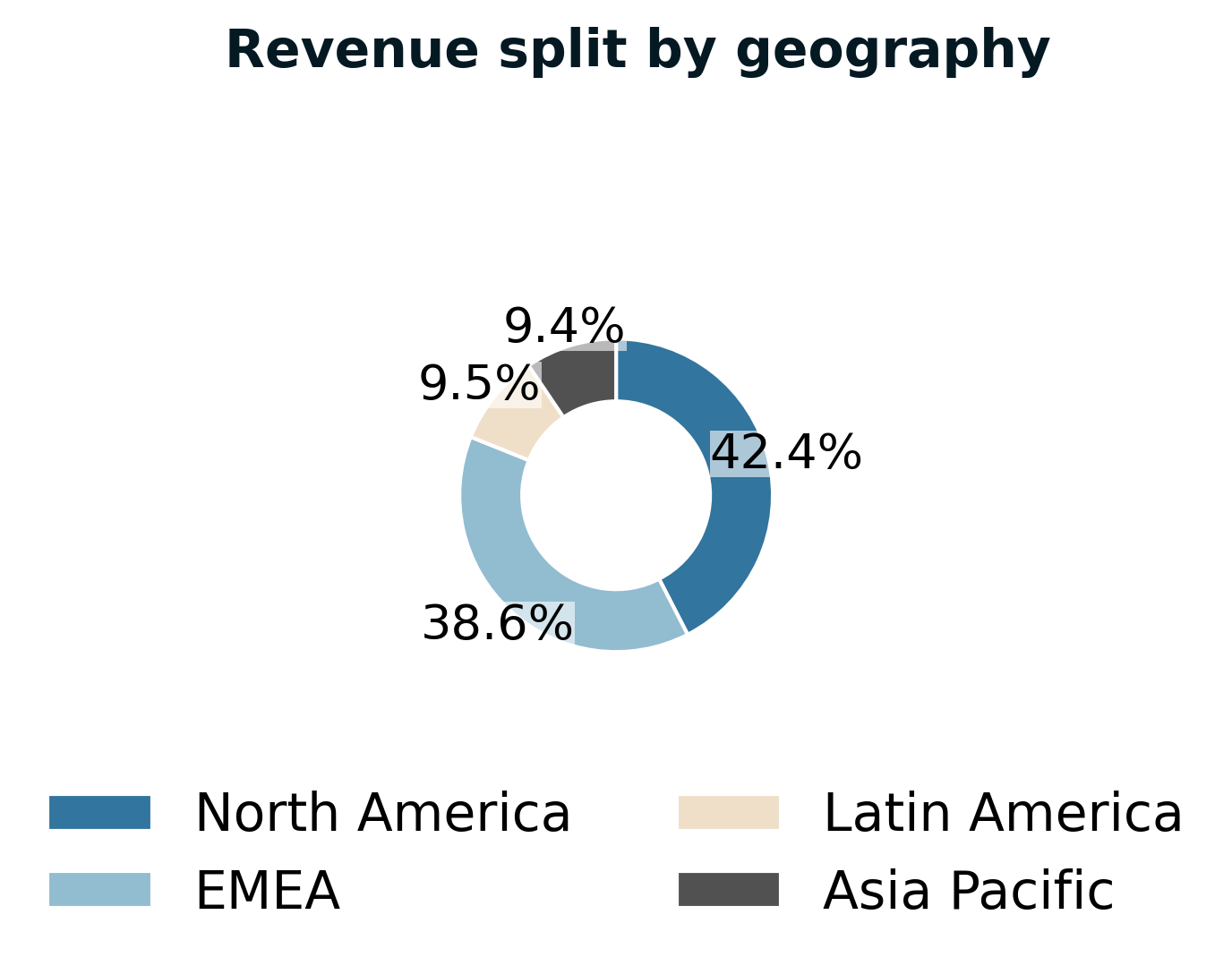

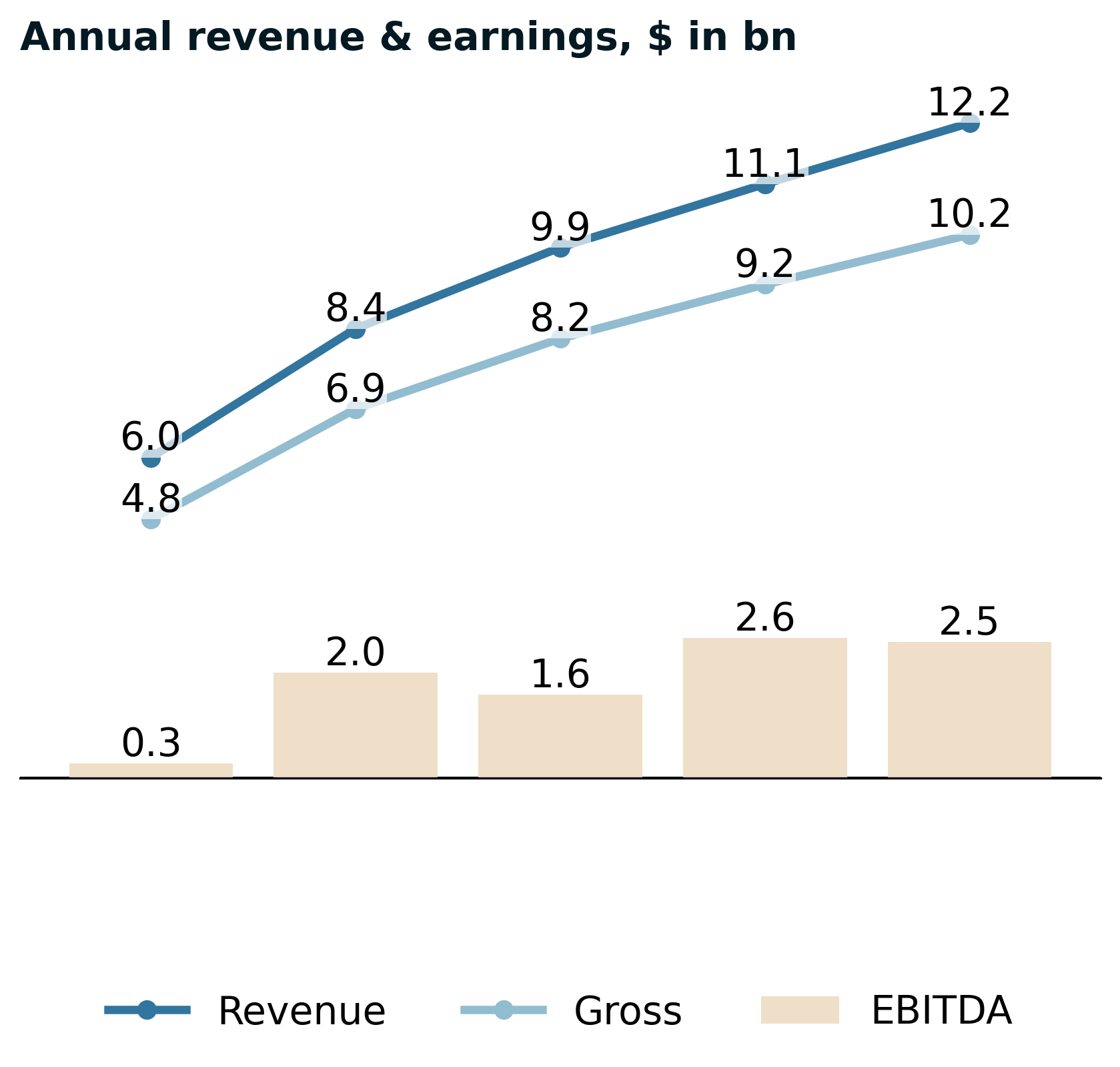

Financial performance

Management on top line and margins

- Nights and Experiences Booked increased across all global regions, driving revenue growth through higher check-in volumes.

- Average Daily Rate expanded modestly, with EMEA demonstrating the strongest pricing appreciation among geographic segments.

- Compensation expense increased and marketing spend elevated, compressing net income despite revenue growth and demonstrating margin pressure from strategic customer acquisition investments.

- Operating expense discipline challenged by strategic investments, though Adjusted EBITDA expanded from check-in volume growth and modest ADR improvement, revealing underlying operational leverage.

Annual report executive recap

Strategy & operating model

- Airbnb rebuilt its technology stack substantially during the year, transitioning to microservices architecture that enabled rapid product iteration while maintaining platform stability and correctness.

- The company launched the Co-Host Network, creating a marketplace-within-marketplace that connected hosts with experienced co-hosts who provided end-to-end listing and booking management services.

Supply chain & operational footprint drivers

- Airbnb operated a global two-sided marketplace connecting guests with hosts across over two hundred twenty countries and regions, creating dual exposure to regulatory environments and operational complexity in each jurisdiction.

- The company substantially completed a technology stack rebuild during the year, transitioning to microservices architecture to enhance scalability and innovation pace while maintaining platform stability.

- Management employed the Live and Work Anywhere policy allowing the vast majority of employees to work remotely, expanding the talent pool beyond physical office commuting range and reducing geographic hiring constraints.

Transactions, portfolio actions & major strategic initiatives

- The company substantially completed a technology stack rebuild during the year, enhancing scalability, reliability, and innovation pace to enable rapid response to changing customer needs while maintaining platform stability.

- Management launched redesigned experiences in May and expanded the Co-Host Network marketplace, creating new revenue streams beyond core accommodations while diversifying the platform offering.

Risk factors & forward-looking signals

- Management acknowledged potential macroeconomic and geopolitical headwinds including inflation, interest rates, foreign currency fluctuations, tariffs, trade controls, and consumer spending pressure, though no material business impact had been observed to date.

- Criminal, violent, or fraudulent host and guest actions directly threatened platform trust, potentially driving user attrition and undermining the core marketplace model dependent on transaction volume.

Earnings call executive recap & narrative evolution

Consistent strategic themes

- Management has maintained unwavering commitment to three growth pillars—perfecting core service, expanding geographically into underpenetrated markets, and diversifying beyond traditional accommodations—with this framework appearing in every call as the organizing principle for resource allocation and execution priorities.

- The platform rebuild narrative has been persistent, with leadership consistently framing the new technology stack as foundational infrastructure enabling faster iteration and future product expansion rather than a one-time project.

Intensifying or reinforced signals

- AI positioning evolved from cautious acknowledgment of early-stage limitations to aggressive investment posture, culminating in high-profile CTO recruitment and explicit framing of AI as existential defense against disintermediation through proprietary data moats.

- Geographic expansion momentum has steadily intensified, with management progressively elevating international markets from background growth drivers to headline success stories, particularly emphasizing Latin America and Brazil as validation of the localization playbook.

Theme drift or shifts in emphasis

- Margin narrative shifted from tolerance for compression due to new business investment toward emphasis on capital-light growth model and stable margin maintenance, suggesting either faster-than-expected profitability in new ventures or recalibration of investment appetite.

- Risk framing moved from specific operational concerns—difficult comparisons, macro uncertainty, geopolitical impacts—to generalized acknowledgment of unpredictability, indicating either improved visibility or deliberate pivot away from forward guidance precision.

Capital allocation signal evolution

- Buyback activity remained consistent throughout but the framing evolved from opportunistic capital return to explicit confidence signal, with management increasingly emphasizing share count reduction as validation of business fundamentals rather than routine capital management.

Risk narrative evolution

- Management progressively de-emphasized near-term headwinds, moving from detailed discussion of comparison challenges and macro uncertainty to minimal risk commentary, suggesting either genuinely improved operating environment or strategic choice to avoid forward-looking caution that might constrain narrative momentum.

Leverage position & capital efficiency

Management on capital structure

- Airbnb attempted to sublease 60% of its total office footprint (0.9 million of 1.5 million square feet), creating substantial lease liability overhang and potential cash flow pressure from negative sublease spreads in distressed commercial real estate markets.

- The company executed aggressive Class A common stock repurchases with substantial remaining authorization capacity, demonstrating confidence in business fundamentals while managing capital structure flexibility despite real estate overcapacity burdens.

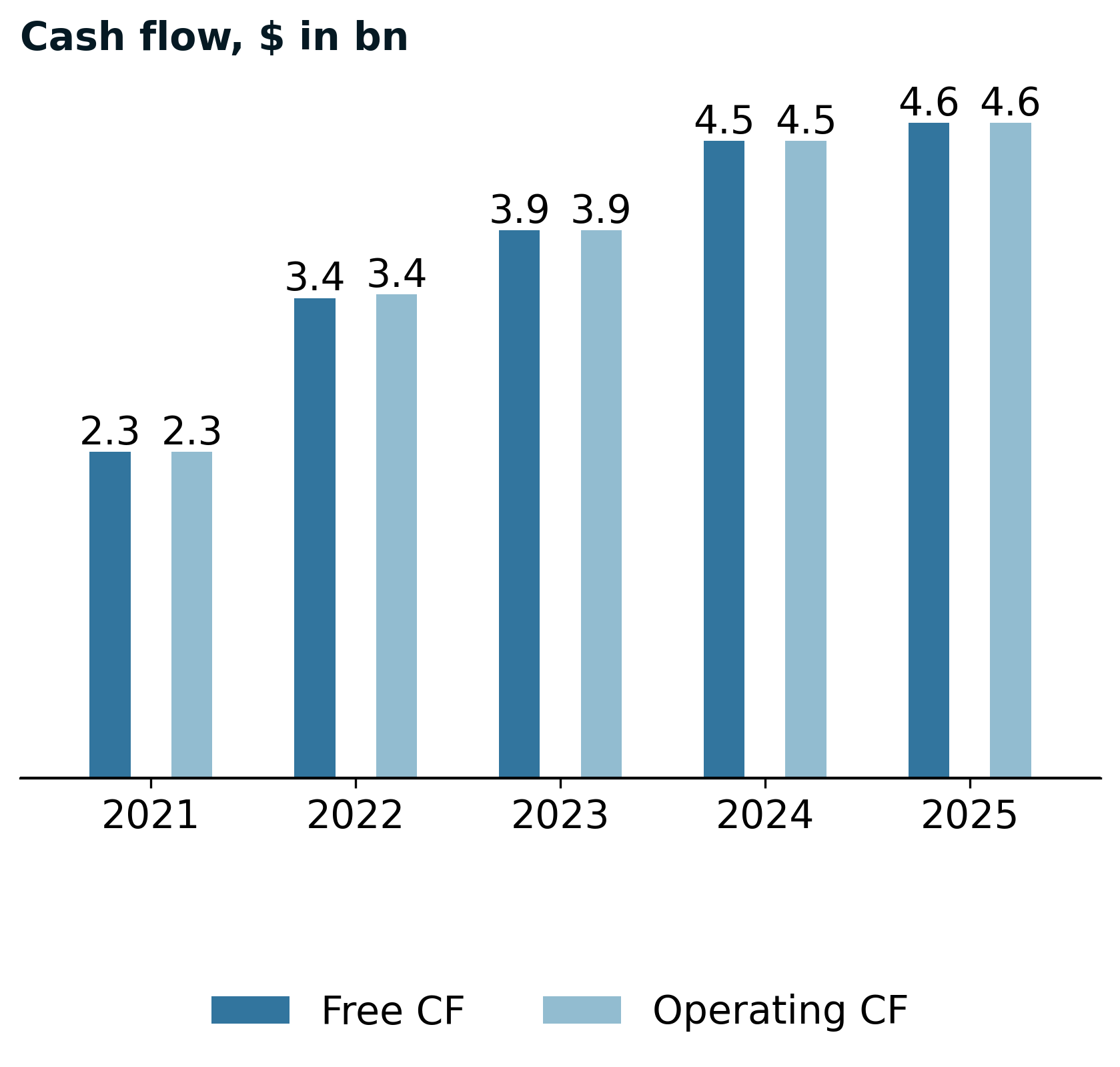

Cash flow and capital allocation

Management on capital allocation

- Operating cash flow improved modestly despite revenue growth, benefiting from favorable working capital dynamics as service fees collected at booking preceded check-in and revenue recognition, creating a timing advantage.

- Management executed substantial Class A common stock repurchases with significant remaining authorization capacity, signaling confidence in business fundamentals and commitment to shareholder returns over alternative capital deployment.

Valuation (2025-12-31)

Disclaimer

This presentation is for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any security or financial product. The content herein is based on publicly available information, believed to be accurate and reliable at the time of publication, but no representation or warranty, express or implied, is made as to its accuracy, completeness, or correctness.

Any opinions, projections, or forward-looking statements expressed in this material reflect our judgment as of the date of publication and are subject to change without notice. Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal.

The recipient is solely responsible for their own investment decisions and should seek independent financial, legal, and tax advice where appropriate. We disclaim any liability for any direct or consequential loss arising from any use of this presentation or its contents.