Capital Discipline Weekly, March 08, 2026

Week of March 01 – March 08, 2026

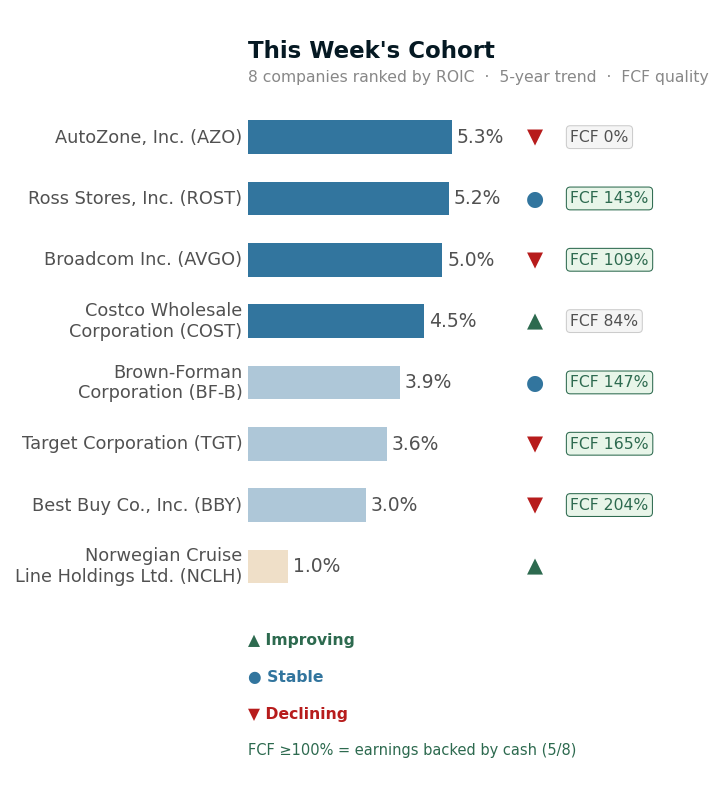

The Cash Machines

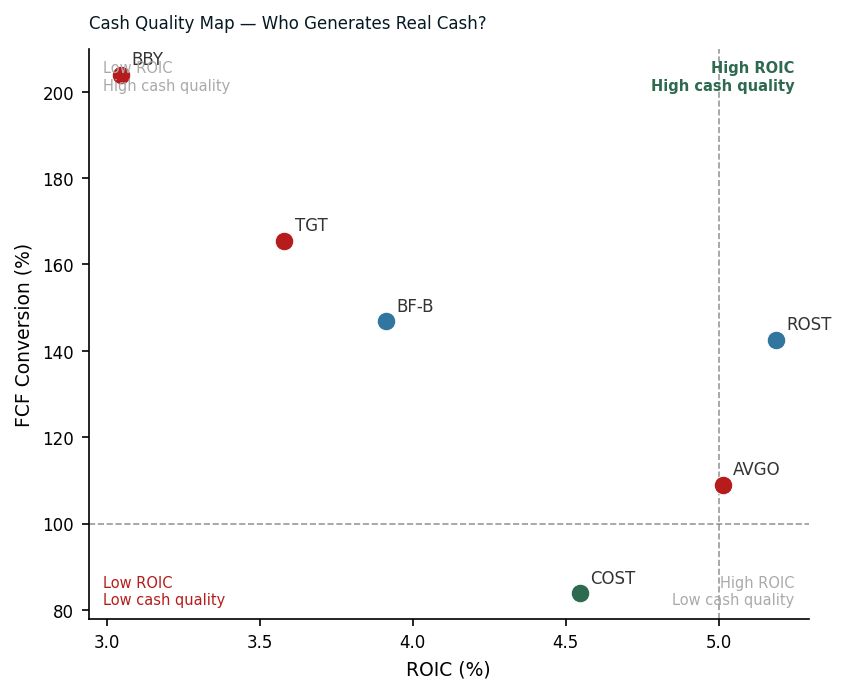

Five S&P 500 retailers and tech giants converted every dollar of earnings into free cash flow this quarter, yet their capital allocation stories diverge sharply. While Ross Stores maintains 5.2% ROIC with methodical store expansion, Best Buy's 3.0% return signals deeper structural challenges despite identical cash conversion efficiency. The disconnect between cash generation and value creation reveals which companies are truly optimizing capital versus merely managing decline.

The Cash Conversion Paradox: When Earnings Don't Tell the Full Story

The divergence between reported earnings and actual cash generation reveals fundamental differences in business model sustainability and earnings quality. Best Buy exemplifies this phenomenon, converting over 200% of its earnings into free cash flow while maintaining a cash ROIC of nearly 20%—dramatically exceeding its accounting ROIC of 3%. This massive conversion ratio stems from the retailer's working capital dynamics, where customer payments arrive before supplier obligations, creating a natural financing mechanism.

Target demonstrates similar cash generation strength, though less pronounced, converting approximately 165% of earnings to free cash flow. The discount retailer's inventory turnover velocity and supplier payment terms create positive working capital contributions that don't appear in traditional profitability metrics. However, Target's cash ROIC of 8.5% more closely aligns with its accounting returns, suggesting less dramatic timing differences than Best Buy.

Ross Stores presents the most balanced profile among retailers, with strong free cash flow conversion around 143% and consistent cash ROIC of nearly 11% that exceeds its accounting returns. The off-price retailer's opportunistic inventory purchasing model creates natural cash flow advantages while maintaining earnings quality.

Brown-Forman's spirits business shows more modest but stable cash conversion at 147%, reflecting the capital-intensive nature of aging inventory and production facilities. The company's cash and accounting returns remain relatively aligned, indicating transparent earnings quality typical of established consumer staples.

Broadcom represents the technology sector's capital allocation complexity, where acquisition-heavy strategies and significant depreciation charges create substantial differences between cash generation and reported profits. The semiconductor giant's cash conversion exceeds 100% despite heavy R&D investments and integration costs.

The cash ROIC premium over accounting ROIC across these companies signals either superior working capital management or potential earnings quality concerns. For long-term holders, cash generation sustainability matters more than quarterly earnings beats—cash funds dividends, buybacks, and growth investments without relying on external financing or accounting adjustments.

Company Spotlights

- Best Buy Co., Inc. (BBY): ROIC 3.0% ↓ Declining, FCF 204%, Volatile consistency

- Target Corporation (TGT): ROIC 3.6% ↓ Declining, FCF 165%, Volatile consistency

- Brown-Forman Corporation (BF-B): ROIC 3.9% → Stable, FCF 147%, Strong consistency

- Ross Stores, Inc. (ROST): ROIC 5.2% → Stable, FCF 143%, Elite consistency

- Broadcom Inc. (AVGO): ROIC 5.0% ↓ Declining, FCF 109%, Volatile consistency

The signal: Despite median ROIC languishing at 4.2%, five companies converting over 100% of earnings to free cash flow reveals a cohort prioritizing cash generation over reinvestment growth.

20+ quarters · 5 metrics · robust trend detection · Full methodology · Subscribe

This analysis is for informational purposes only and does not constitute investment advice.