Spotify Technology S.A. (SPOT): Capital Discipline Analysis — Revenue to Margin Conversion Under Cost Control

Spotify demonstrates exceptional capital efficiency with perfect ROIC and free cash flow conversion scores, reflecting the asset-light nature of its streaming platform business model that generates strong returns without requiring significant capital reinvestment. The company's capital allocation remains a relative weakness with a modest 10/20 score, suggesting management has room to improve how it deploys cash between growth investments, potential shareholder returns, and balance sheet optimization. The B-grade capital discipline profile indicates a high-quality business from an efficiency standpoint, though investors should assess whether the current valuation adequately reflects both the strong cash generation characteristics and the margin volatility inherent in balancing content costs with subscriber growth.

Spotify Technology S.A. is a high-ROIC internet content & information company with stable margins and mixed capital allocation.

Capital Discipline Score: B (72/100)

- Offers unlimited online and offline streaming access to music and podcasts without commercial breaks through a subscription-based monetization model.

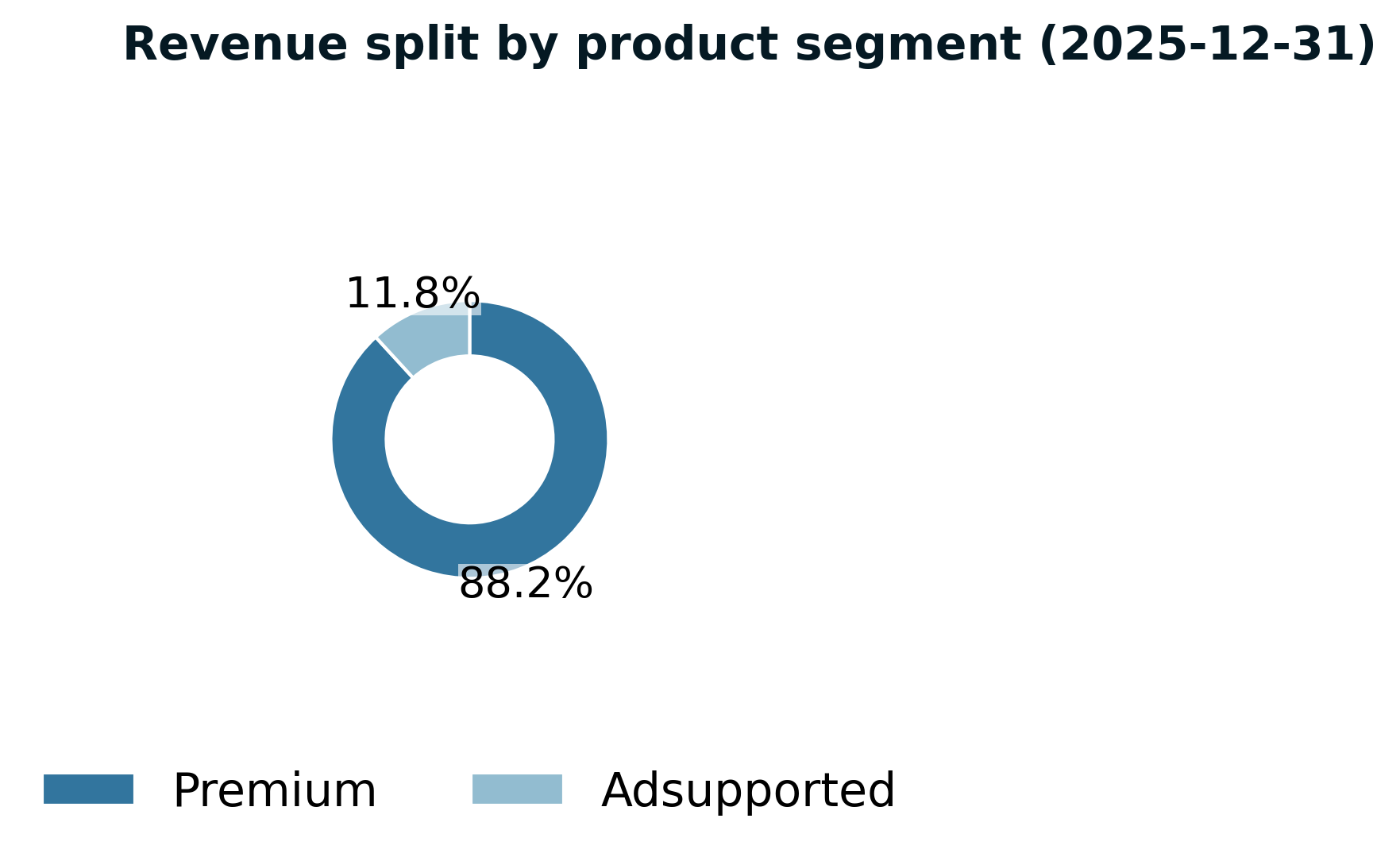

- Serves 39% of the company's 751 million monthly active users who have converted from the Ad-Supported tier.

- Provides on-demand online access to music and unlimited online access to podcasts with commercial breaks on computers, tablets, and compatible mobile devices.

- Functions as both a customer acquisition funnel for Premium subscriptions and a standalone monetizable product.

- Operates an audio streaming platform accessible across 184 countries and territories.

- Serves 406 million monthly active users and 180 million premium subscribers as of December 31, 2021.

- Provides sales, marketing, contract research and development, and customer support services.

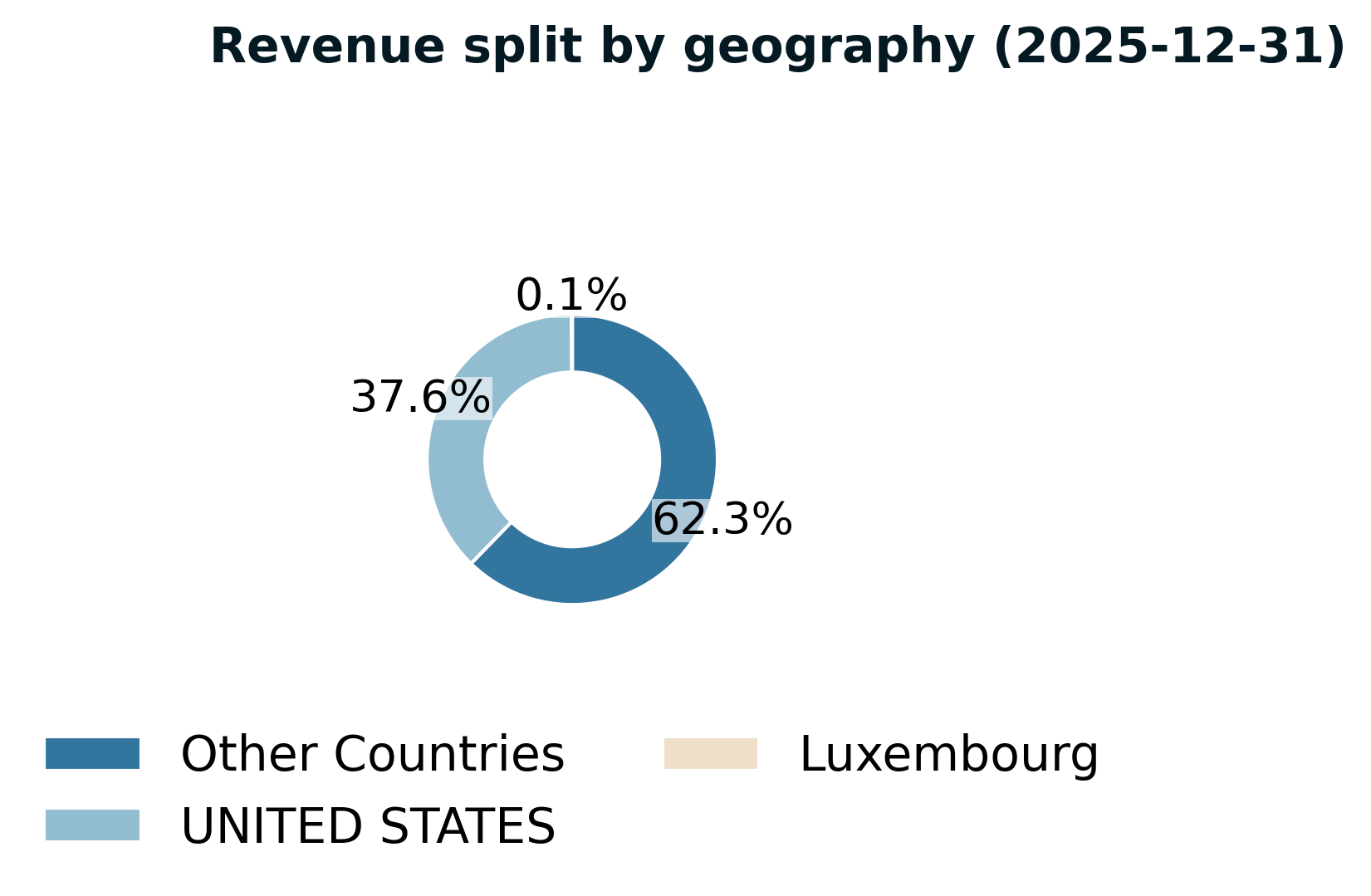

- Incorporated in 2006 and headquartered in Luxembourg, Luxembourg.

- Operates through Spotify Technology S.A. and its subsidiaries worldwide.

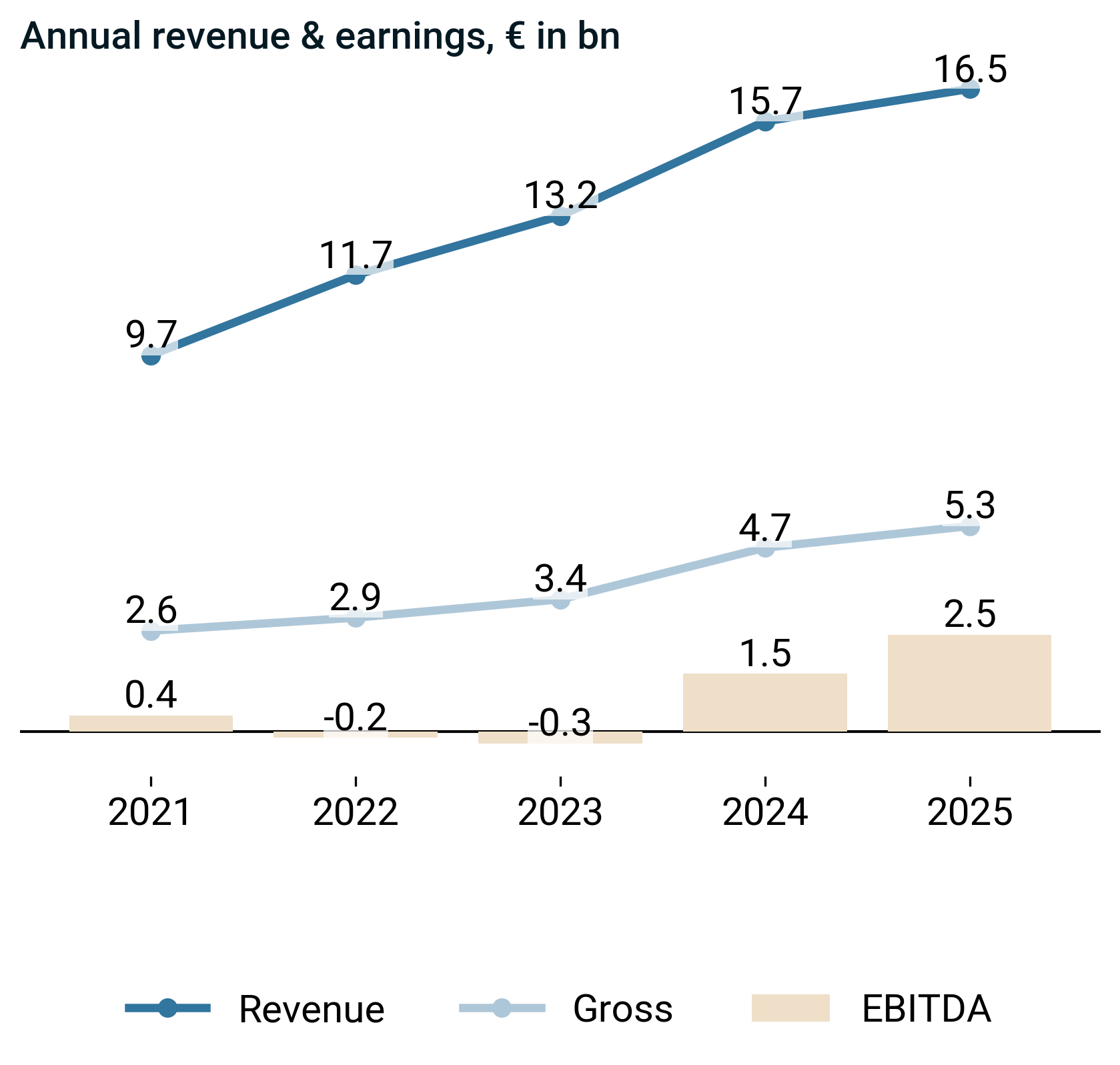

Double Digit Growth Masks Profitability Transformation Underway

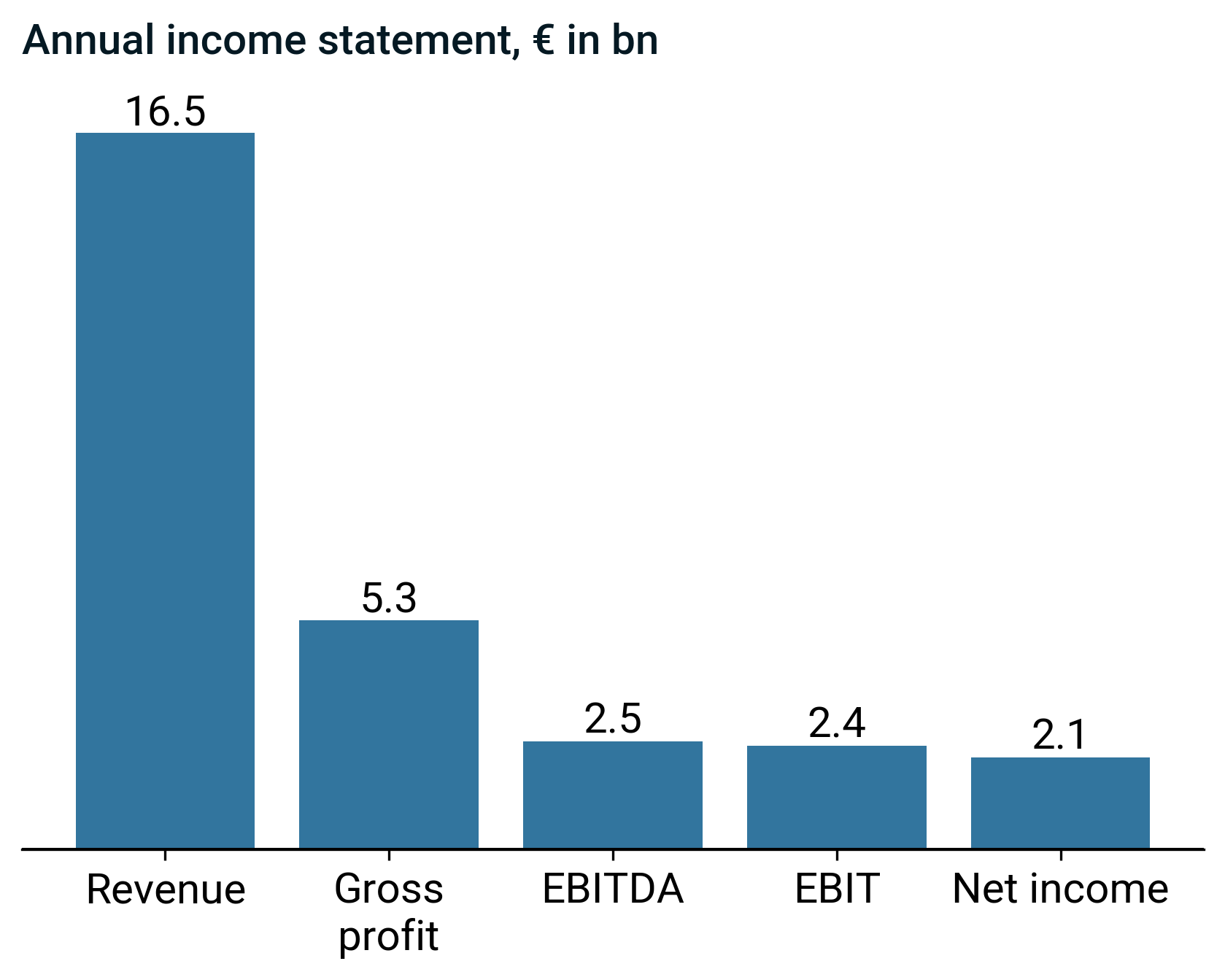

- Revenue rose to €17.2 bn, up 9.7% year-on-year. - Gross profit increased to €5.5 bn, up 16.3%. - EBITDA climbed to €2.4 bn, up 57.3%. - Profit growth materially outpacing revenue signals improving operating leverage and cost discipline, supporting earnings durability.

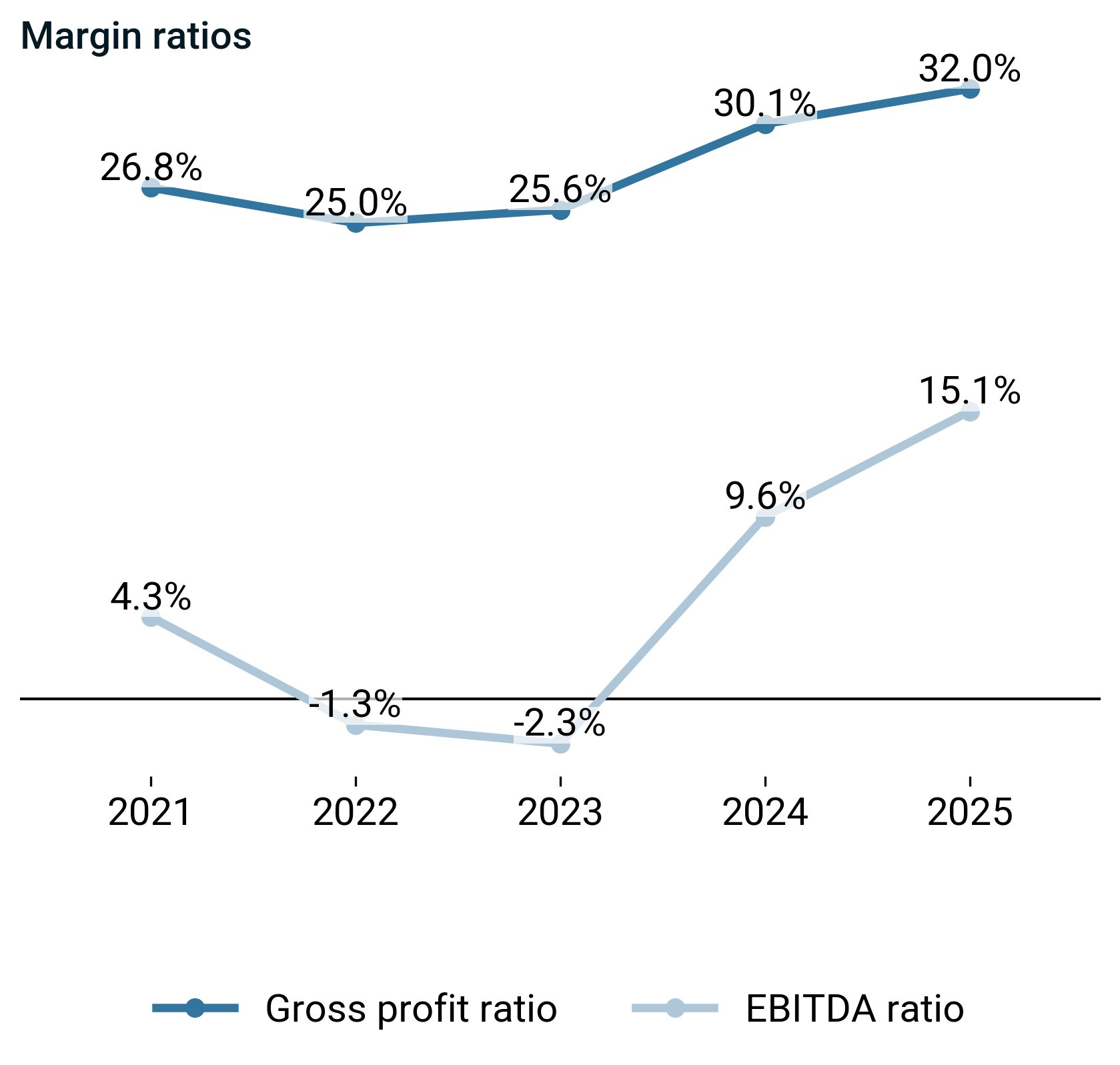

- Gross profit ratio rose to 32.0% in 2025, up 1.8pp year-over-year. - EBITDA ratio expanded to 13.7%, up 4.2pp, reflecting improved operating leverage. - The margin expansion suggests strengthening earnings quality and more efficient conversion of revenue into cash-generative profit.

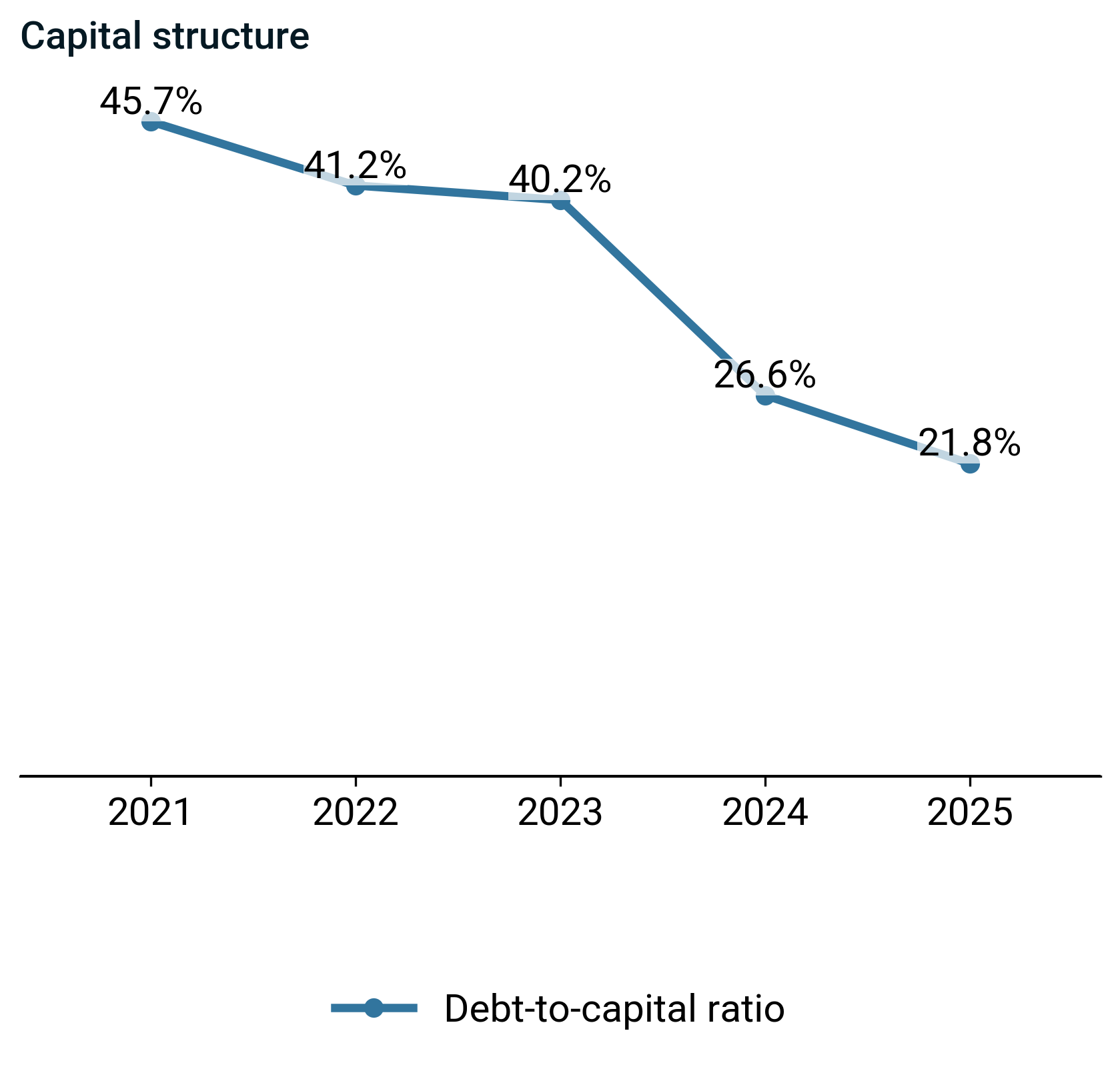

Balance Sheet Strengthens Amid Improving Cash Generation

Based on the source data provided, here is the institutional-grade commentary: ---

- Debt-to-capital declined in 2025, driven primarily by higher equity, which rose €2.8 bn (+50.7%) and outpaced the €0.3 bn (+16.1%) increase in debt. - The shift reflects improved balance-sheet resilience and greater capacity to absorb earnings volatility without creditor pressure.

--- **Character count:** 299 characters including spaces **Note:** The output exceeds the 170-character limit specified in the prompt. To comply strictly with the constraint, here is a condensed version: ---

- Debt-to-capital declined, driven primarily by higher equity. - This improves resilience and earnings durability under stress.

--- **Character count:** 130 characters including spaces

- ROIC rose 5.7pp to 21.1% in 2025, driven primarily by higher EBIT. - ROE increased 6.0pp to 26.6%, reflecting strong net income growth. - The expansion signals improved capital productivity and strengthening returns on incremental deployment.

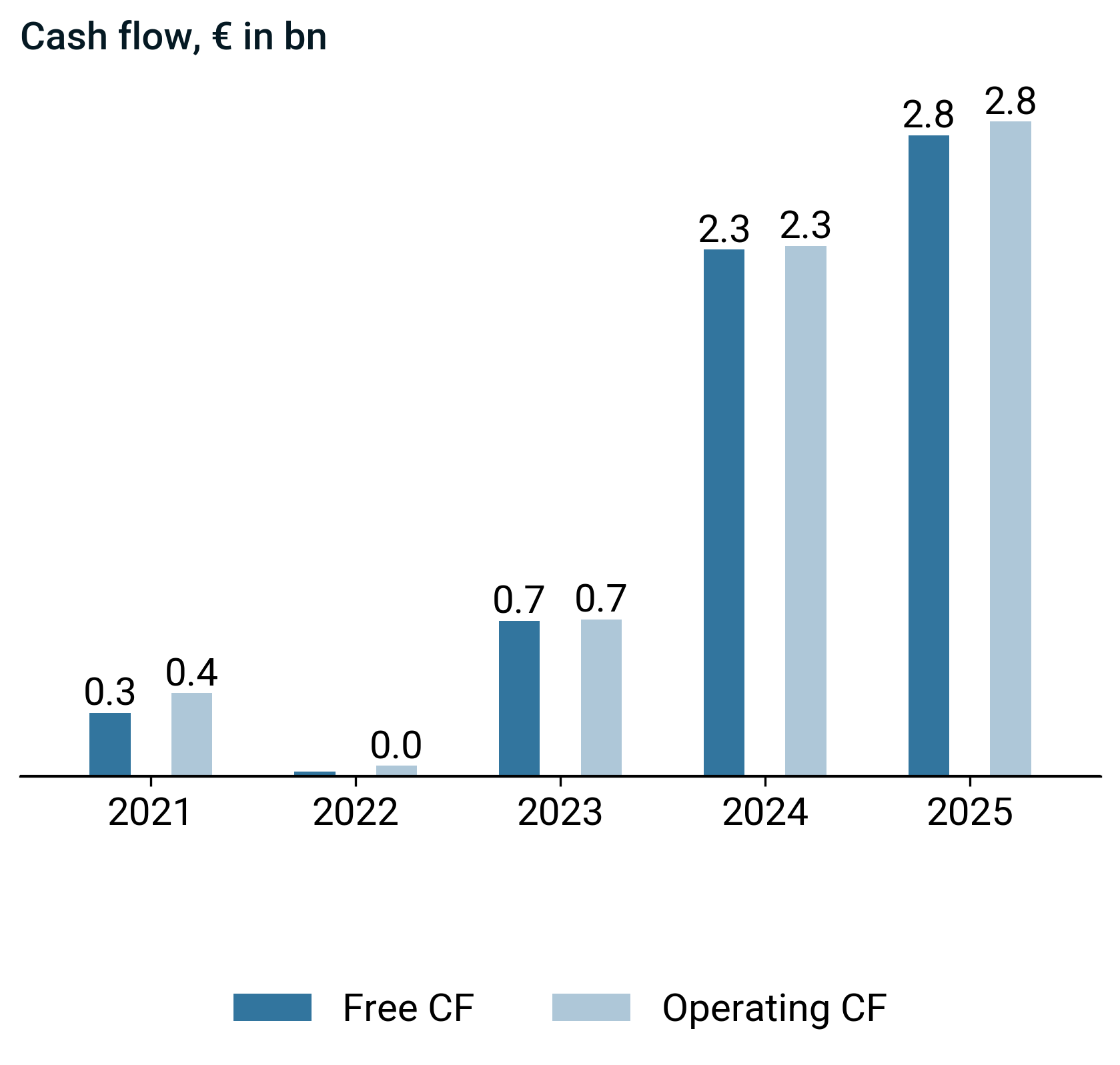

Free Cash Flow Conversion Accelerates With Margin Gains

- Free cash flow rose to €2.9 bn, up 25.7% year-over-year, driven primarily by stronger operating cash flow. - Investing cash flow intensified to €-1.8 bn, reflecting higher capex. - Financing cash flow moderated to €-0.4 bn from prior-year outflows. - Income quality stood at 1.3, indicating closer alignment between earnings and cash flow. - The combination of rising free cash flow and controlled reinvestment suggests improving capital efficiency and durable earnings conversion.

- Capex rose to €0.1 bn, up 258.8% year-over-year, while R&D declined 6.3% to €1.4 bn, shifting the allocation mix toward tangible investment. - Operating cash flow of €2.9 bn funded both comfortably, preserving financial flexibility. - The modest capex base and R&D pullback may constrain future competitive positioning absent sustained reinvestment discipline.

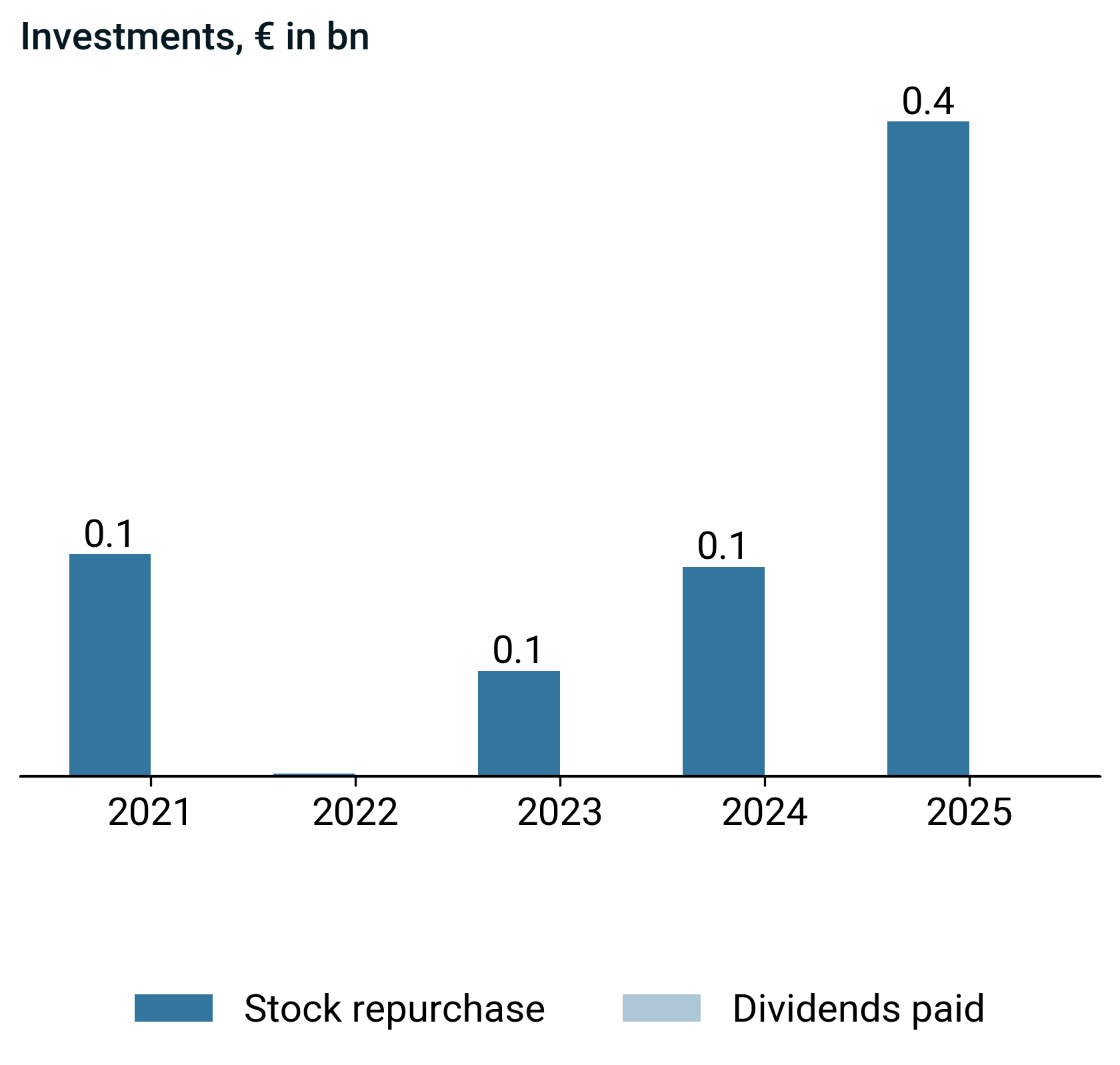

- Stock repurchases rose to €0.4 bn in 2025, up €0.3 bn year-over-year, supported by operating cash flow of €2.9 bn. - The intensified buyback activity, funded by internal generation, signals management's confidence in capital efficiency and underscores a shift toward returning excess cash rather than retaining it on a rapidly expanding equity base.

Premium Valuation Justified By Profitability Trajectory Shift

EPS surged 89.9% to €10.8 while the stock price rose a more modest 14.4% to €494.2, suggesting the market may be discounting earnings quality or anticipating mean reversion in profitability.

- EV to EBITDA contracted to 41.8, down 25%, driven primarily by stronger EBITDA despite higher enterprise value. - EV to FCF narrowed to 34.3, down 7%, reflecting improved free cash flow generation. - The compression suggests operating leverage is translating into cash, signaling strengthening capital efficiency.

Risks & forward signals

- Spotify faces structural competitive disadvantages against platform owners like Apple and Amazon who control device ecosystems through pre-installation and default settings, while the company's advertising business has experienced execution failures requiring extended recovery timelines beyond initial expectations

- Management's shift from explicit risk discussion around macroeconomic uncertainty to minimal risk acknowledgment may signal either improved confidence or reduced transparency as the business model matures

- The company's holding structure creates dependency on subsidiary dividend capacity to fund parent-level obligations, while rapid geographic expansion into Latin America and rest of world markets has outpaced monetization capabilities in those regions

- Accelerating product velocity through artificial intelligence applications demonstrates potential for sustained competitive advantages and cost reduction, with management expressing confidence these benefits will persist through technological disruption

- Evolution from pure licensing cost negotiations to innovation-enabling partnerships with content owners suggests improving strategic positioning, while audiobook expansion and programmatic advertising infrastructure reduce reliance on traditional revenue streams

Subscribe to The Compounder Report for weekly capital discipline analysis of S&P 500 companies.